The name 1911 Gold is no coincidence. In 1911, Duncan Twohearts discovered gold in the Rice Lake Greenstone Belt in Manitoba, Canada, marking the beginning of this district’s legendary history. After over 20 years of development, the first mine shaft was commissioned in 1932, and remains in use today. At its peak, the district produced roughly 1.3 million ounces of gold at an exceptional grade of 9 g/t, making it one of Canada’s most notable high-grade gold mines.

Rice Lake is also situated in one of western Abitibi’s most prospective greenstone belts, sharing hallmark characteristics with world-class gold districts such as Red Lake and Timmins, laying the foundation for long-term potential.

Over the decades, the mine changed hands several times due to gold price cycles and infrastructure challenges:

1980s – Rea Gold invested CAD 280 million to rebuild surface facilities, the shaft, and the mill, while initiating deep exploration. However, low gold prices and high capital expenditure led to bankruptcy before production.

2004–2015 – San Gold developed the Hinge, Cohiba, and 007 deposits, reaching an annual production peak of 80,000 ounces in 2011 and a market capitalization above USD 1 billion. However, a production-at-all-costs approach, lack of grade control, and falling gold prices drove costs higher, ultimately leading to bankruptcy in 2015.

By 2018, the region had produced approximately 2 million ounces of gold, with over 1 million ounces of potential resources still untapped.

*Notably, the macroeconomic environment has improved significantly: while San Gold peaked under gold prices of USD 1,200–1,400/oz, current prices have stabilized above USD 2,000/oz. Manitoba’s political and mining policy stability, secure tenure, and reliable infrastructure, power, and labor support provide a favorable backdrop for 1911 Gold’s restart.

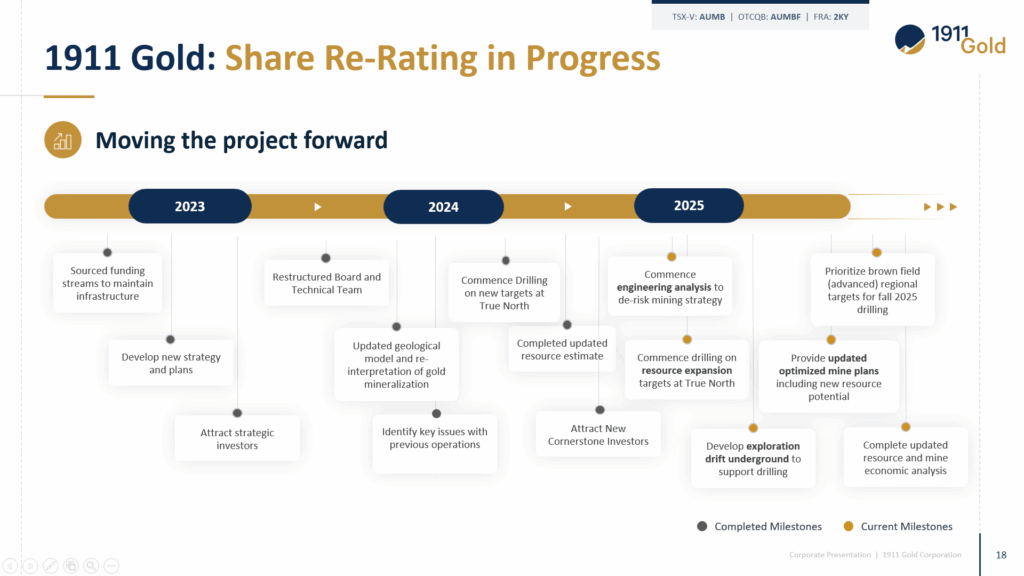

After Klondex divested its assets in 2018, 1911 Gold acquired the True North Project, inheriting well-developed infrastructure and the largest gold resource potential in the region. At the time, the company held approximately USD 9 million in cash, and later raised USD 17 million via a Charity Flow-Through financing. This funded a tailings reprocessing project, which successfully operated from 2019 until it ceased in 2022.

This reprocessing phase not only generated cash flow but also allowed the team to reacquaint itself with Rice Lake’s geology and infrastructure. In 2023, the company officially announced plans for underground exploration and mine restart, marking a step toward “true production.”

Today, 1911 Gold benefits from strong shareholder support: renowned resource investor Eric Sprott increased his stake to 17.2%, providing both endorsement and market confidence.

*More strategically, 1911 Gold has inherited a fully permitted mill infrastructure. This means that the company does not need to reapply for complex permitting processes and can start production immediately when needed, greatly shortening the restart cycle and reducing uncertainty. This is extremely rare among North American mining companies and is an important barrier to entry for 1911 Gold.

The True North Project is 1911 Gold’s core asset, with a clear roadmap:

Exploration & Expansion

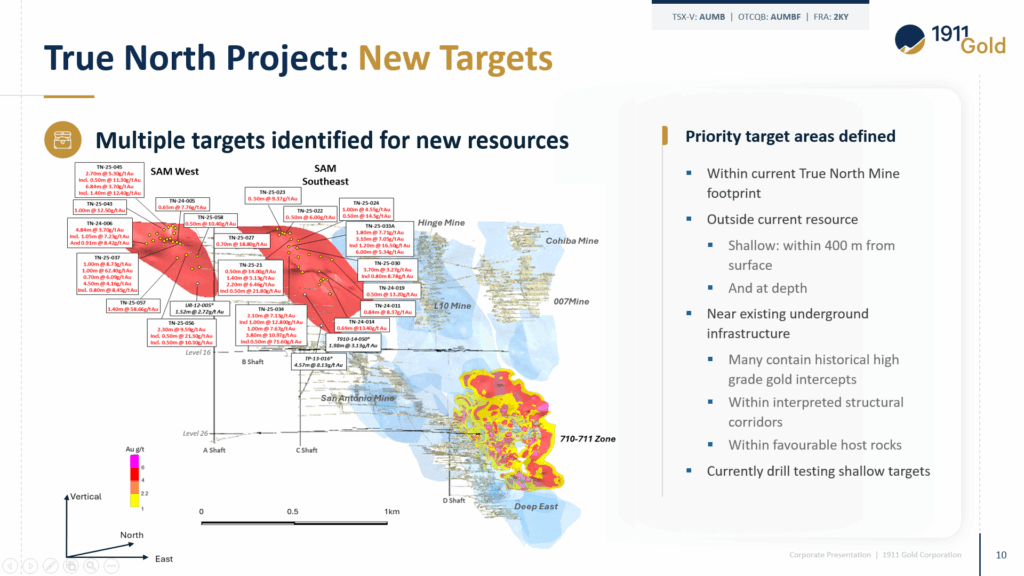

Key surface targets are SAM West and SAM Southeast, parallel vein systems. The goal is to deepen exploration to extend deposit depth and expand future resources.

Underground exploration has been underway for several months, with drilling entering its core phase over the next five weeks.

👉The company’s immediate focus is a 1,500-meter underground drill program, scheduled for late September 2025 — the first underground drilling in 8 years. This program is designed to unlock over 1 million ounces of identified gold resources. Most of the recently raised capital will be allocated to this effort, providing robust validation of resources ahead of the PEA.

Bulk Sample Validation

Two bulk sample targets will be tested at the 16th level of the mine, using delineation drilling to reduce geological uncertainty.

Delineation drilling is scheduled to begin in January 2026, followed by Bulk Samples starting in April 2026 and expansion in September–October.

This batch is expected to yield ~15,000 ounces of gold at an estimated cost of USD 1,800/oz over six months.

*True North’s advantages are significant: existing infrastructure—mill, shaft, and camp—is ready for immediate use, avoiding hundreds of millions in upfront capital; the project’s location in the historically productive Rice Lake Greenstone Belt (over 2 Moz historic production) positions it alongside world-class gold districts; and a multi-pronged exploration strategy balances short-term production with long-term expansion.

These measures demonstrate 1911 Gold’s prudent, low-capital approach to restarting production, avoiding the mistakes of San Gold’s past overproduction strategy.

Beyond its operational blueprint, 1911 Gold has a series of major catalysts that could drive market revaluation:

Ongoing drilling results to be released regularly through April 2025.

PEA (Preliminary Economic Assessment) scheduled for December 2025.

Delineation drilling to be completed in January 2025.

Two bulk sample tests starting in April 2025.

Updated mineral resource estimate to follow.

Commercial production targeted for early 2027.

Each milestone represents not only a step toward commercialization but also a potential trigger for share price appreciation and market re-rating.

Past operators failed for distinct reasons:

Rea Gold: excessive capital expenditure beyond what gold prices could support.

San Gold: production-focused strategy neglecting grade control and precise drilling, causing both resource and economic decline.

1911 Gold differentiates itself through:

Low capital risk: infrastructure is largely complete, requiring minimal upfront investment.

Scientific approach: delineation drilling ensures precision and prevents resource dilution.

Strategic shareholder support: Eric Sprott’s substantial stake enhances market credibility and liquidity.

Favorable gold cycle: long-term high gold prices support the restart of small, high-grade operations.

*Combining favorable macro conditions (high gold prices, stable policy, prime location) with micro-level operational discipline, 1911 Gold is executing a measured restart, creating an unprecedented investment window.

For investors, 1911 Gold offers:

High resource certainty: proven historic production and remaining resources indicate significant potential.

Light capital intensity: complete infrastructure enables faster, lower-risk restart versus building new mines.

Clear strategic path: Tailings → Exploration → Bulk Sample → Full Production, a logical and trackable progression.

Positive market signals: entry of renowned investors such as Eric Sprott signals strong confidence.

1911 Gold’s re-rating potential becomes evident when compared with peers. For example, Canadian Gold Corp, also located in Manitoba, holds only ~300,000 ounces of resources. Despite higher grades, its remote location and lack of infrastructure mean everything must be built from scratch. Yet, McEwen Mining is considering a merger at a valuation of USD 120 million.

By contrast, 1911 Gold controls over three times the resources, with all infrastructure fully permitted and ready for production, yet trades at a market cap of just USD 60 million. This stark contrast highlights the undervaluation and re-rating potential of 1911 Gold.

If the bulk sample tests proceed as planned, the resulting revenues are expected to fund the restart of production independently, without the need for additional equity financing. This significantly reduces dilution risk, preserving upside for current shareholders.

Equally important, 1911 Gold was spun out of Klondex in 2018 at an initial price of CAD 0.60 per share, meaning there are no cheap “legacy shares” in the structure. Management’s holdings come entirely from market purchases or financing participation, aligning their incentives directly with shareholders and reinforcing long-term value creation.

*Combining the long-term stability of gold prices, Canada’s stable policy and mining environment, and a scientific exploration strategy, 1911 Gold is creating a high-quality investment opportunity that combines historical heritage with future potential.