In the outlook for crude prices, a crucial factor is how far US shale oil production can grow. The shale revolution has transformed global oil markets over the past decade, reversing the long decline in US output, challenging Opec’s influence, and helping to trigger the plunge in prices that began in 2014. It has meant windfalls for oil consumers, and some painful adjustments for producers.

The track of the number of active rigs and oil production shows the huge productivity gains that have been made. A rush to drill in shale formations such as the Eagle Ford in Texas and the Bakken in North Dakota was followed by a flood of production, which mostly held up even after most rigs stopped running in 2014-16.

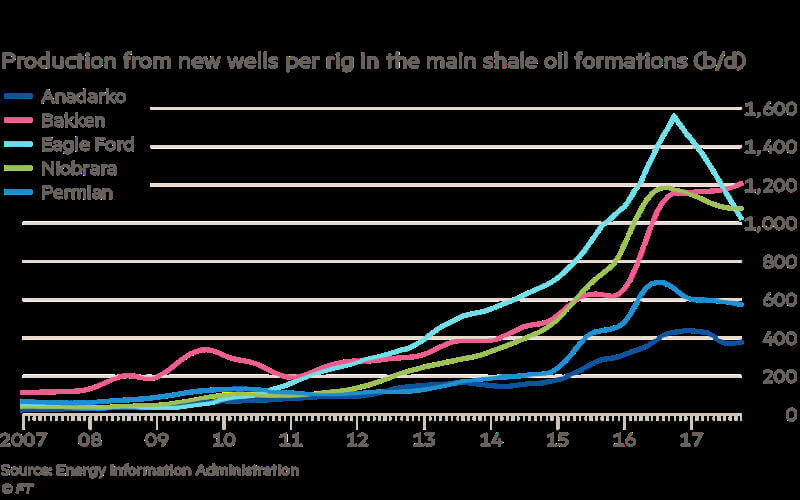

Over the past year, however, the productivity gains seemed to have slowed considerably, suggesting that the revolutionary era for progress in shale is over. In the Eagle Ford shale, productivity — as measured by production from new wells per active rig — has been falling. Those productivity data from the Energy Information Administration are an imperfect measure, however. For a start, they do not take into account the extent to which companies are drilling wells and then deliberately not bringing them into production as they wait for higher prices. (These are known as DUCs, or Drilled but UnCompleted wells.) So what can we say about the true picture of productivity in shale?

One issue is the time it takes to drill the wells. The recorded efficiency of rigs improved dramatically over 2013-16, in part because of the spread of pad drilling: running multiple horizontal wells off from a single site, or pad, to cut down the time spent moving the rigs. Recently, however, the rate of improvement appears to have slowed, especially in the Eagle Ford shale and the Williston Basin, which includes the Bakken formation. Wells are generally getting longer, so companies may still be going faster in terms of feet per day, even if they take the same time to drill each well. But it does look as though that particular source of productivity gains is not what it was.

Throughout its existence, the shale oil industry has consumed cash. Companies have been unable to cover their drilling costs from their incomes, and have needed constant infusions of debt and equity financing. They have had little difficulty in raising that money, in part because investors wanted to share in the productivity miracle that the companies represented. If the miraculous days are over, and a more humdrum reality is setting in, will investors still be prepared to back the industry so willingly? Already equity raising by US exploration and production companies has slowed sharply this year. Plenty of attractive investment opportunities still exist in shale: internal rates of return of 30 per cent and higher are available in the Permian Basin, according to S&P Global Platts Well Economic Analyzer. Will there be enough of those attractive opportunities to keep US oil production rising, as the government’s Energy Information Administration and others expect? The industry says yes, but the drilling and productivity numbers will be worth watching closely over the months to come.

Source: www.ft.com