In the gold market, two types of companies typically capture the most investor attention:

“0 to Producer” – companies that transition from exploration to production, creating a clear path for market re-rating as they move from zero to cash flow.

“Production Growth” – established producers that expand output and optimize operations, increasing scale and market value.

West Red Lake Gold (WRLG) stands out as a rare representative of the second category.

At present, new gold producers just entering the production stage are exceptionally rare. WRLG is not bringing its flagship new gold mine into production right now, but also has a defined expansion plan and multi-asset development strategy. This combination offers attractive potential. For emerging gold miners, as production stability is demonstrated and operational risk declines, the market often rates companies as reliable operators. If a company then charts a path to growth, capital tends to flow in ahead of results, driving valuation re-rates that can be multiples of the move in the price of gold itself. Historically, growth-oriented gold producers have consistently outperformed indices such as GDX and GDXJ — and WRLG is entering this scarce, high-growth window today.

WRLG is among the very few “newly producing and scalable” gold companies in the market, a scarcity factor that naturally channels investor capital into the stock.

The Beginning (2014)

The modern story of the Madsen Mine began in 2014 when Pure Gold drilled ~180 km and successfully defined the project. Before production was declared, the company’s market cap reached as high as US$1.2B, once again bringing the Red Lake district back into the spotlight.

Pure Gold’s historic valuation provides a benchmark for WRLG, while also demonstrating the market’s recognition of Madsen’s potential.

The Turning Point (October 2022)

Pure Gold ultimately went bankrupt due to several critical missteps:

Limited operational expertise to transition from exploration to production, which led to cutting corners during construction and operations.

Insufficient understanding of the orebody and mining design, leading to a disconnect between plans and reality, with risk escalating.

Technical execution shortfalls: drill spacing of ~20 meters failed to capture narrow, high-grade veins; underfunding delayed key processes, resulting in high costs and low recovered grades.

While Pure Gold failed, Madsen retained its full resource potential — and left behind valuable lessons for its successor.

Taking over Madsen, WRLG adopted a “Show Me” strategy — proving credibility through results:

Comprehensive Review – re-assessing geological models and engineering assumptions to ensure alignment with on-site reality.

Technical Precision – reducing drill spacing to 7 meters ahead of final mine design, improving accuracy in identifying narrow, irregular veins.

Bulk Sampling – validating models through test mining, which confirmed strong consistency and reliability.

Disciplined Ramp-Up – upfront investment in personnel and equipment allowed a smooth ramp-up from January to July, producing nearly 10,000 oz of gold.

Stable Operations – mill throughput sustained at 650–800 tpd.

Risk Management – meticulous oversight of mining sequences, faces, costs, and capex, ensuring no “cut corners.”

Transparency – regular updates with milestones and production data to reinforce market confidence.

Madsen had deposit and much of what’s needed to mine it — WRLG’s job was to prove it could operate the mine reliably and scale it. The successful bulk sample provided the validation investors needed, driving a valuation re-rate and confirming the company’s production capability.

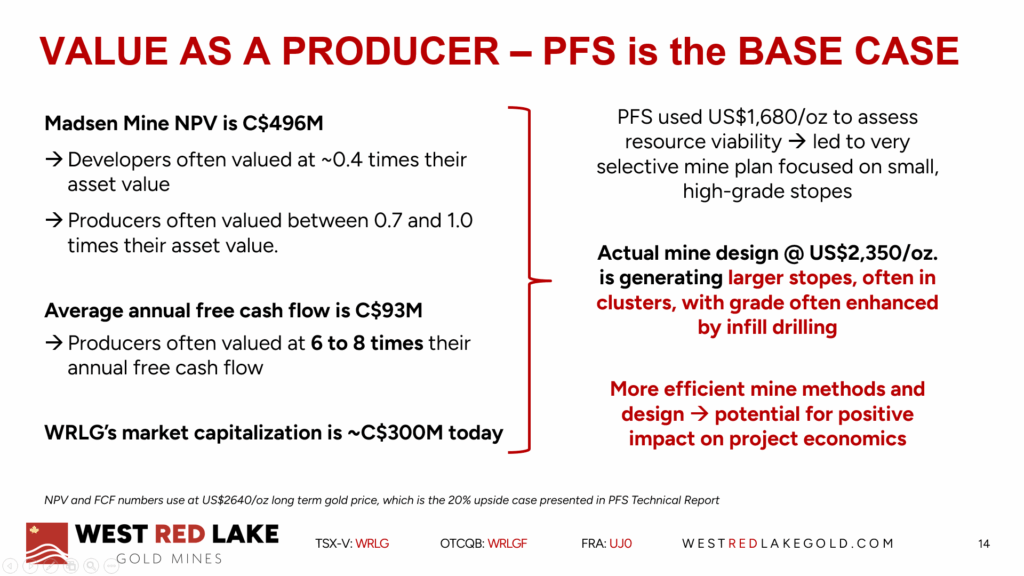

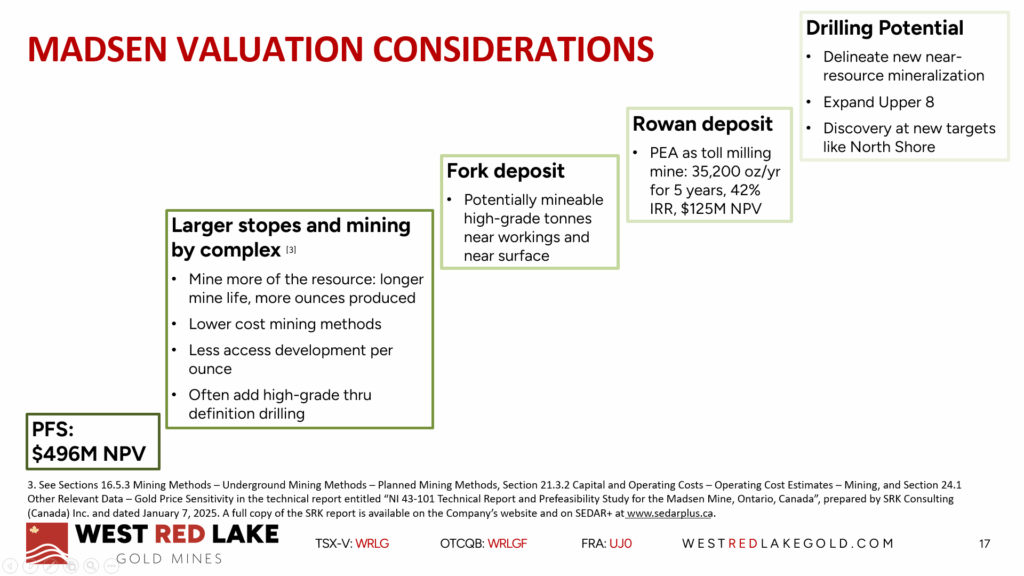

Madsen PFS (Jan 2024) projected ~67,600 oz gold per year for six years — but this is a conservative plan for how to mine the much larger Madsen deposit.

The study was conservative because it used a gold price of only US$1,680/oz and so considered only the highest-grade zones, excluding significant tonnage that makes sense to mine at higher gold prices.

With spot gold comfortably above US$3,000/oz, WRLG is doing final mine design at US$2,350/oz. As a result, more of Madsen’s mineralization is coming into the mine plan. This has the potential to lift output, increase mine life, reduce unit costs, and improve cash flow and profitability for years to come.

At higher gold prices, WRLG can unlock more ounces, lower costs, and drive stronger free cash flow and margins.

Beyond Madsen, WRLG controls other important assets:

Rowan Project – small but high-grade deposit 80 km away by road, expected to deliver ~35,200 oz annually for five years. A Pre-Feasibility Study (PFS) is targeted within 6–8 months, as part of creating a comprehensive production plan for West Red Lake Gold’s operations in Red Lake and their growth trajectory.

Fork Deposit – shallow, high-grade, and located near Madsen. With low development costs and easy integration, it provides quick incremental growth.

Together, these assets establish WRLG as a multi-mine growth platform, making the re-rate logic clearer — not just expansion at one mine, but diversified, scalable production with cumulative cash flow growth.

Upper 8 Zone – limited drilling (17 holes) has already returned grades up to 44 g/t, pointing to potential high-grade discoveries.

Other underexplored areas across the land package provide long-term optionality and discovery leverage.

Scarcity Value – Red Lake is world-renowned, and producers that are both newly online and scalable are exceptionally rare. WRLG is uniquely positioned.

Technical & Operational Discipline – tighter drill spacing, validated bulk sample, stable mill operations, and upfront investment should ensure reliability.

Multi-Asset Growth – Madsen, Rowan, Fork, and additional exploration zones create a diversified growth engine.

Clear Investment Case – rising production, higher gold prices, and investor interest turning toward gold can combine into a powerful value-creation cycle.

Upside Optionality – exploration targets such as the Upper 8 Zone could add new high-grade ounces.

WRLG has proven its production capability and re-rate potential through the successful restart of Madsen, while simultaneously building a multi-asset growth pipeline at Rowan, Fork, and other zones.

Overall:

Production, cash flow, and earnings are on an upward trajectory.

Unit costs are expected to decline, while higher-grade development could enhance returns.

WRLG is a rare “newly producing and scalable” gold company.

For investors, WRLG represents more than just a stable new producer — it offers a quantifiable, high-visibility growth story backed by historical benchmarks and future expansion opportunities.