New Opportunity Alert: Emergent Metals Corp. (TSX-V:EMR)

The resource exploration markets, much like the overall market, have been rather sleepy since the pandemic bull run we saw about 2 years ago.

Such is why one small cap mining company in particular had modeled their business to stay resilient during rough market conditions, yet are poised to shine when the storm passes.

By seeking promising projects within proven jurisdictions, this company not only holds 2 coveted properties with great intrinsic value of their own, but have taken advantage of a “buyers market” in the resource sector to acquire a handful of other properties within Nevada and Quebec that their CEO has been actively flipping; enhancing the company’s cash position and regulating their burn rate simultaneously.

Suggested Opportunity

Emergent Metals Corp. (TSXV: EMR, OTCQB: EGMCF, FRA: EML, XBER: EML)

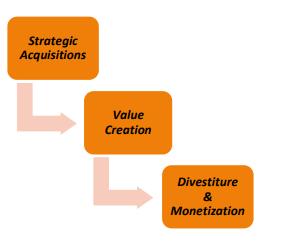

Emergent is a gold, silver, and base metal exploration company focused on Nevada and Quebec. The Company’s strategy is to look for asset acquisitions in a buyer’s market, add value to the acquisitions through computerization and remodeling of historical exploration data, new exploration, and application of modern geophysics, and seek divestitures through sale, joint venture, option, royalty, or other business transactions to advance our projects and create value for our shareholders.

With a great corporate strategy and impressive collection of properties, this company is hot on our radar coming into the new year…

Emergent Metals Corp (TSXV:EMR) (OTC: EGMCF) (EUR: EML) is a gold, silver, and base metal exploration company focused on Nevada and Quebec.

The company states that its strategy is to “look for asset acquisitions in a buyer’s market, add value to the acquisitions through computerization and remodeling of historic exploration data, new exploration, and application of modern geophysics, and seek asset divestitures through sale, joint venture, option, royalty, and other business transactions to advance our projects and create value for our shareholders.”

Focusing on Politically Stable Jurisdictions

Emergent’s foothold over politically-stable regions Nevada and Quebec is no accident – both regions have a rich history of mining, hosting world class deposits and mines, bearing excellent geology and potential for:

● Discovery,

● Acquisition,

● Enhancement, and

● Divestiture of Projects.

In the Fraser Institute’s 2020 Survey for Attractiveness for Mining Investment, NV was ranked #1 and QC was ranked #6.

Dissecting EMR’s Acquisition Strategy

Having a basket of properties provides advantageous diversification for EMR. CEO David Watkinson, also known as the Warren Buffet of mining, has a proven track record of not only exploring and developing select properties for future value creation, but also divesting certain properties for cash flow and corporate enhancement as the opportunity arises.

As stated by EMR, their business strategy is to “to hit singles, doubles, triples, and home runs with multiple opportunities, rather than focus on one core asset and the goal of taking it to production.”

A few of many notable transactions by Emergent’s frontman David Watkinson:

East West Property, Quebec

● Acquired for $400,000

● Sold to O3 Mining Inc, for $750,000 cash and 325,000 shares of O3 (worth ~$750,000)*

Troilus North property (Quebec)

● Acquired for $650,000

● Sold to Troilus Gold Corp. for $250,000 cash and 3,750,000 shares of Troilus Gold

(worth ~$2,625,000)*

Stewart & Rozan property (Northern B.C.)

● Acquired for $1 in a property swap

● Sold to Ximen Mining Corp. for $100,000 cash and 1,275,000 shares of Ximen and

1,275,000 warrants of Ximen at $0.45 (worth ~$1,147,500)*

*Figures reflect share values of purchasing companies on date of press release

This sound strategy allows EMR to focus on what it does best: finding the most promising undervalued assets, conducting early stage exploration work, and negotiating with larger mining players for deals that would benefit shareholders.

In turn, larger mining companies benefit from their relationship with EMR by simplifying their process of finding new projects to acquire and develop.

Speaking of larger mining players…

EMR’s JV with Rio Tinto’s Subsidiary Kenecott Exploration:

The New York Project

EMR’s standout project is the New York Canyon Property (“NYC”), an early-stage exploration property located about 30 miles east of Hawthorne, Nevada.

EMR has an earn-in, option and joint venture agreement with Kennecott Exploration, a subsidiary of mining giant Rio Tinto. Kennecott can earn up to a 75% interest in the Property by completing up to US$22.5 million in expenditures.**

**Full agreement outlined in corresponding press release

NY Canyon consists of 21 patented claims and 417 unpatented claims and has undergone geochemical sampling, geophysics, metallurgical test work, and over 139,000 feet of drilling as of present. The three known exploration targets on the southern portion of the NYC property include Longshot Ridge, Copper Queen, and Champion.

The kicker? Mr. Watkinson snagged this property for a US$250,000.

With EMR’s joint venture agreement involving Kenecott, this means that EMR does not need to spend additional capital on exploring the property. If exploration leads to positive results, EMR can sell its remaining interest to Kennecott for a positive return.

With US$22.5 million being spent for 75% interest in NY Canyon, this lifts EMR’s portion of the project at US$7.5 million, a 2900% return on investment.

For context, Emergent’s market cap is currently under US$5 million, proving that with NY Canyon alone we are looking at an undervalued company with plenty of upside.

There is a reason David Watkinson is referred to by many as the Warren Buffet of mining.

Consult your advisor about this opportunity and keep an eye on Emergent Metals Corp. (TSX-V:EMR) (OTC: EGMCF) (EUR: EML)!

Disclaimer: NAI is being compensated for this content. Materials contained in this content are for information purposes only and is not intended to constitute an offering of securities in any jurisdiction. Nothing on this content should be construed as an offer, solicitation or recommendation to buy or sell products or securities.

Copper

Gold

In-Depth Analysis

Industrial Metals

Mining

Precious Metals

Silver