District Metals Corp. (TSXV:V.DMX. Nasdaq: DMXSE SDB)

Advancing the Largest Undeveloped Uranium Deposit in the World

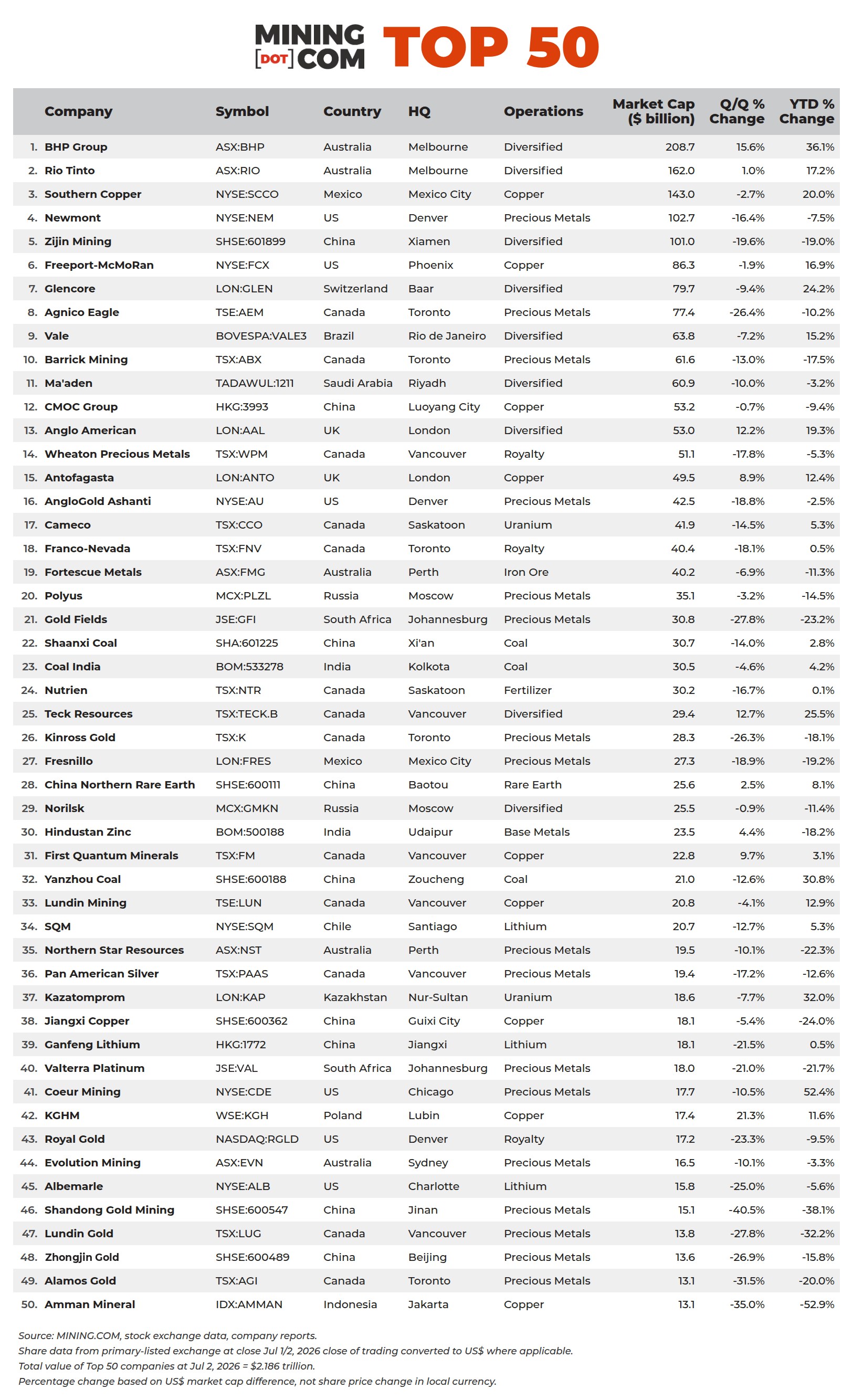

In the first half of 2026, the global mining capital markets experienced a crucible of extremes. After a brief rally in the first quarter following the outbreak of the U.S.-Iran conflict, the world’s 50 largest mining companies suffered a sharp valuation correction in the second quarter. According to the latest MINING.COM ranking as of early July, the combined market capitalization of the world’s 50 most valuable miners fell to $2.19 trillion, wiping out $228 billion from the prior quarter, with year-to-date gains shrinking precipitously to just $22 billion.

At the root of this turmoil lies a deep pullback in gold. After hitting an all-time high of $5,589 per ounce in late January, gold embarked on a five-month decline, officially breaking below the psychological $4,000 level in the final week of June—a nearly 30% drop from its peak. The underlying driver is not a failure of gold’s traditional safe-haven logic, but rather a clear chain of transmission from geopolitical conflict to energy prices, and from there to a reshaping of monetary policy expectations: the U.S.-Iran conflict disrupted shipping through the Strait of Hormuz, widening energy supply gaps and fueling global inflation expectations.

Markets pivoted abruptly from pricing in Fed rate cuts to “rate-hike trades,” with a strengthening dollar exerting fundamental downward pressure on gold. This macro narrative shift turned the gold sector into the second quarter’s hardest-hit area, with precious metals companies suffering a “blanket blow.” China’s Shandong Gold saw more than 40% of its value erased, plummeting 16 places in the ranking.

However, not all were losers. As gold’s luster faded, a cohort of traditional diversified mining giants—led by BHP, Rio Tinto, and Anglo American—staged a “return of the kings” this quarter. BHP, in particular, rode its unparalleled portfolio resilience to a 16% counter-cyclical market cap gain, adding approximately $28 billion to reclaim $209 billion in total value. This clearly signals that in an environment of heightened macro uncertainty, the defensive value of asset diversification is being repriced.

Meanwhile, copper’s strategic position remained solid. Despite sharp price volatility, copper’s investment thesis was reinforced by robust downstream demand and persistent supply disruptions. Zijin Mining, though facing share-price headwinds, posted a first-half profit forecast of approximately RMB 39.1 billion, up roughly 68% year-on-year—underscoring its ability to weather market cycles. CMOC also reported a first-half profit increase of over 70%, confirming the industry-wide trend of “higher volumes and higher prices” for copper products.

The shifting fortunes in the mining rankings reflect a core market narrative: valuations driven by liquidity are deflating, while pricing logic grounded in supply-demand fundamentals and corporate fundamentals is regaining dominance. The lithium sector’s “disconnect” is particularly telling—despite a sizable year-to-date increase in lithium carbonate prices, the market caps of major producers shrank instead, indicating that market wariness of prior overhyping and longer-term supply pressures has overtaken near-term price signals. The rare earth sector tells a similar story: even with government-backed orders in hand, companies like MP Materials remain well below the cutoff for inclusion, leaving state-backed China Northern Rare Earth as the sector’s sole representative in the top 50.